Even though the company is making money, it still goes bankrupt. When doing business, not only look at “profit”.

The ability to collect money is more important than the ability to make money!

If you are a start-up company, you don’t have much cash on hand at the beginning. At this time, you have to deal with all the daily expenses and expenses. If you still need to use credit sales, you will “not receive money”. Then it is very likely that you may accidentally fall into the risk of bankruptcy if you don’t have enough cash, and you may even be unable to survive.

Black Word Bankruptcy

Every time I chat with the owners of small and medium-sized enterprises, everyone exchanges their management methods, opinions on the market, and various ups and downs in life. Of course, the most important purpose of doing business is to make money, so the topic of whether to make money or How to make money and obtain better profits is always the most important in the discussion process. Although it is very important to discuss whether and how to make money. Not making money will certainly make people worry and fear, but the most regrettable or embarrassing thing is that despite making money, in the end, the business has to be terminated and faced with the fate of bankruptcy. This is the “black letter bankruptcy” that we often hear.

The black word is a term in accounting, that means that the company is making money and profits, so the black word bankruptcy means that the company is profitable but closed down.

Looking into the reason, the fact is that the company has made money, but a lot of the money has not been received. In other words, these incomes are still “accounts receivable” and have not been turned into cash and returned to the company.

Under this situation, the company’s costs and expenses continue to occur, cash keeps flowing out, but the money owed by customers never comes in, so in the end the cash “cannot make ends meet”, the company will be unable to sustain itself and declare bankruptcy.

Some people may say that if you do not do business on credit, you will not be able to grow your revenue or even retain customers. Therefore, “accounts receivable” is a “necessary way” and a tool that is necessary for doing business. If you use If this tool is removed, it will make doing business more difficult.

What must be particularly clarified here is that accounts receivable is indeed a necessary tool for doing business, and we also recognize its value, but it is important not to let accounts receivable “get out of control” ; that is to say, To ensure that the money in accounts receivable can be “recovered” and “recovered immediately”, we can avoid the dilemma of clearly making money but having no money to pay or even going bankrupt. Not to mention that some accounts receivable cannot be collected at all, so it is more practical not to do this kind of business.

As mentioned in the previous class, although accounts receivable is a good tool for doing business and is a common practice in the industry, how to use it still depends on the results of “negotiation” and “choice” between the buyer and the seller; if you want to avoid If you make money but are at risk of going bankrupt, then the most important thing is to control the “accounts receivable level”, that is, the number of accounts receivable. Here are three directions that everyone can use as a reference benchmark:

- Cash level 2. Money collection speed 3. Spending speed

Three reference benchmarks to avoid going bankrupt despite making money

1. Cash level

The company has a lot of cash: the level of accounts receivable is high

The company has little cash: the level of accounts receivable is low

When a company has a lot of cash, it can certainly increase its accounts receivable level. The reason why we need to realize accounts receivable as soon as possible is not only because we are afraid that customers’ debts will turn into bad debts, but the most important key is that we need cash turnover and cash to pay all the costs of daily operations. Therefore, if the cash stock is high enough, there is no rush to convert accounts receivable into cash as soon as possible, and the level of accounts receivable can be higher than that of ordinary companies.

For example, TSMC’s accounts receivable were 100 billion in the first quarter of 2019 and increased to 140 billion in the fourth quarter. Although it seems that the accounts receivable increased by 40%, the average amount of accounts receivable remained the same. It has about 500 billion in cash. In other words, TSMC has a large enough cash level to support the growth of its accounts receivable, so it is relatively risk-free.

Therefore, the more cash a company has, the more capable it is of using credit sales to expand its business, because increasing the level of accounts receivable will not bring actual operational risks to it.

On the other hand, if it is a start-up company, it does not have much cash on hand at the beginning, and at this time it has to deal with all the daily expenses and expenses. If it still needs to use credit sales so that it “cannot receive money”, then It is very likely that you may accidentally fall into the risk of bankruptcy if you don’t have enough cash, or even survive.

I often share with small and medium-sized business owners that accounts receivable is a “choice”. When you don’t have enough cash, it will not be a better “choice”;

At this time, you can choose customers who are willing to trade with you in cash, customers who can pay you as soon as possible, or even customers who are willing to pay you cash in advance, so that the cash on hand can be accumulated slowly and safely.

When your cash grows larger and larger, you can “choose” to enlarge your accounts receivable and choose customers with more credit sales but good credit.

2. Money collection speed

Collect money quickly: accounts receivable level is high

Slow collection of money: low level of accounts receivable

The second key factor that will affect whether the level of accounts receivable should be kept relatively high or low is the speed of collecting money quickly or slowly.

This concept is very simple. If your customer does not make a cash transaction, but settles the money quickly, although there is an account receivable on the account, the account receivable stays for a very short time, and it will be cleared all of a sudden. It will be converted into cash. Although it seems that the level of accounts receivable is high it is equivalent to cash.

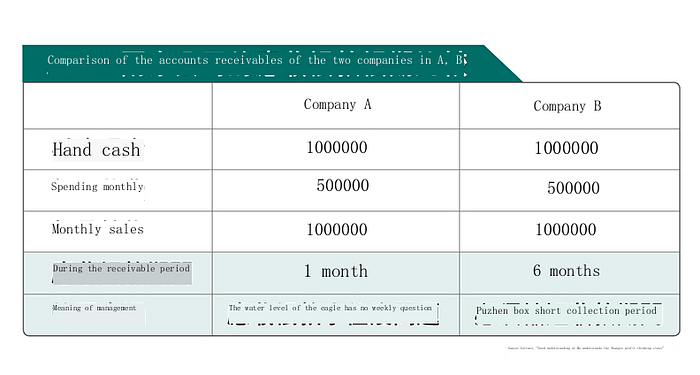

On the contrary, if the accounting period of accounts receivable is very long, it means that there is no cash inflow during this period, and it cannot cover your daily expenses, but you must have cash to survive, so this kind of collection Transactions with long receivables can only account for a small part of all your transactions, which means your accounts receivable level cannot be too high. Here are two examples of companies A and B:

Assume that companies A and B both have 1 million in cash on hand, their monthly expenses are 500,000, and their monthly sales revenue is also 1 million; the only difference is that if companies A and B want to sell on credit, The account period given by the customer is one month for Company A to collect, while Company B needs six months.

In this situation, we can see that even if Company A puts its monthly sales of 1 million on its account as accounts receivable, the cash will be recovered in one month anyway, and the 1 million in cash on hand can also cover the first month’s sales. 500,000 in expenses, so the accounts receivable level remains at 1 million, which is no problem at all.

On the other hand, if Company B trades all its monthly sales income on credit, it will not receive any cash for six months. At this time, the 1 million he has on hand can only cover two months. Expenditures were stretched after two months. Under this situation, it is inevitable to lower the level of accounts receivable and conduct some transactions in cash to meet daily expenses.

This also shows why the faster you collect payments, the more you can increase the level of accounts receivable.

3. Speed of spending money

Slow spending: High levels of accounts receivable

Spend money fast: Accounts receivable is low

The last key factor that will affect the level of accounts receivable is the speed of spending money.

If you spend money slowly, it means that the urgency of the need for cash is not very high. In this case, if the level of accounts receivable is higher and cash collection is slightly slower, the impact on operations will not be so great.

But if you spend money very quickly, it means that you have a very strong need for cash. If the level of accounts receivable is too high the collection speed is too slow, and you cannot keep up with the speed of cash flow out, then you must control it well. Manage and reduce the amount of accounts receivable. Let’s take the same example of two companies, A and B:

Assume that Company A and Company B both have cash on hand of 1 million, and their monthly sales are also 1 million. If they want to sell on credit, the accounts receivable period is both 2 months; the only difference is that Company A’s monthly expense is 50 thousand, while Company B’s is 800,000; that is, Company A’s expenses are less than those of Company B, and the monthly cash outflow rate of Company B is faster than that of Company A.

Under this situation, we can see that even if Company A turns all its monthly sales income into accounts receivable through credit sales, the 1 million cash on hand can cover two months of expenses without any problem, and two Cash will come in after months, and there won’t be any cash shortage. In other words, it can maintain the level of accounts receivable at 1 million.

However, under the same circumstances, Company B needs to spend 800,000 per month, so the 1 million in cash on hand cannot support two months of expenses, so it is bound to be unable to sell all sales revenue on credit. In other words, In other words, B’s accounts receivable level must be less than 1 million.

Therefore, only by reducing the company’s expenses, or the speed at which it spends money, can it increase the company’s accounts receivable level.

Therefore, saving costs and reducing expenditures, in addition to increasing the company’s profits, also increases the company’s competitiveness in doing business. If the money is spent less and the speed is slower, we can give customers more opportunities to sell on credit. As long as they have good credit, our business can be bigger.

Nowadays, many small companies don’t even have offices. This can not only reduce office rent, fixed expenses for water, electricity, and telephone bills, but even employee transportation expenses. Overall, it can reduce the speed of company expenses. Through the study of this class, we know that this is another opportunity to strengthen the competitiveness of doing business.

Therefore, if we regard accounts receivable from credit sales as a business tool, we must make good use of this tool, which can help us make money without the risk of cash shortage or bankruptcy.

Under this situation, it is necessary to carefully consider the “cash level”, “speed of collecting money” and “speed of spending money” to adjust and balance the number of accounts receivable, while taking into account both profit growth and financial security.

Thanks for your reading. Share your thoughts, and suggestions, and help shape a better experience. If you find it inspiring, share it with your friends give it a ‘clap’ and follow. Let’s build something great together — drop your comments below!